Covid new reality

According to the latest estimates, more than 190 million jobs will be lost due to the Coronavirus, and for the first time after the 2008 crisis, the planet will enter a new recession. The drastic fall in family income will bring with it an irremediable crisis of default and liquidity that will fully impact on the cash flow forecasts of companies.

Enabling companies with analytical capabilities to anticipate possible cases of default, modelling the best actions to be taken by the team, can lead to a dramatic change in the success rates of recovery.

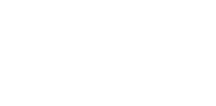

Experts point out that in Spain, each percentage point increase in unemployment increases bank default by 0.75%, understood as the resulting quotient between doubtful risks (unpaid loans) and total risks (total loans granted). After the 2008 crisis, banks have focused much of their efforts on reducing this ratio to below 5%. Currently the value is 4.83% (homogeneous values to those obtained in 1987). In the fourth quarter, the ratio is expected to reach between 8% and 10%, which will mean that the unemployment rate will rise from at least 13% at the end of 2019 to close to 20%.

This new crisis will destroy not only the jobs most historically affected in recessions, such as temporary jobs, or those associated with construction, but it will also cause people who under normal circumstances would never lose their jobs to end up falling into unemployment. This fact, together with the lack of liquidity of the families, will generate both a rise in default, and an increase in the drop of products and services that are not strictly necessary: the identification of customers with specific financial needs will become more important than ever, for this, providing financial departments with analytical tools can increase the opportunity of recovery by up to 70%.

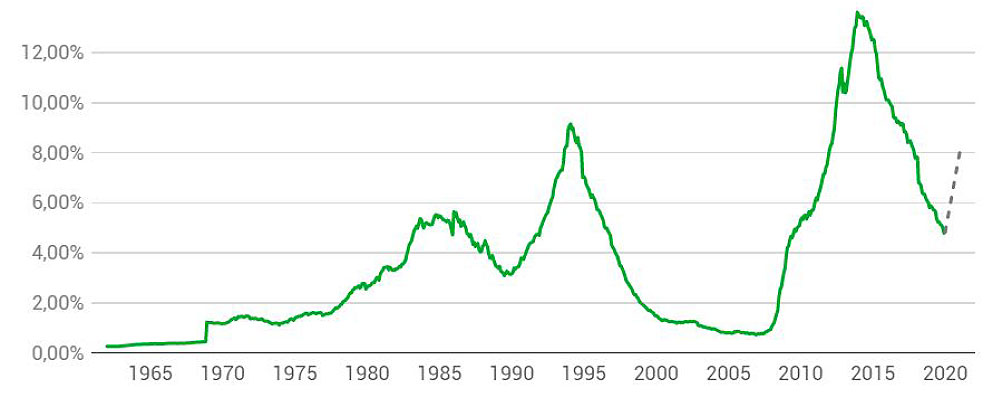

Transformation to guarantee BAU

In this situation, companies are faced with different fundamental needs:

- To guarantee the continuity of the business, stabilizing the processes of current recoveries overloaded or not prepared for new needs. Having an external workforce available on a temporary basis, agile and flexible, to stabilize the business is critical.

- Identify customers who are in default due to the crisis, but who can be expected to recover their ability to pay when the business returns to normal.

- Enable predictive models to anticipate default and prescriptive models to customize the most effective recovery actions for each customer, making the success rate of current processes more efficient.

- Combine the previous points in processes developed on the basis of good practices to homogenize and make recovery actions more efficient.

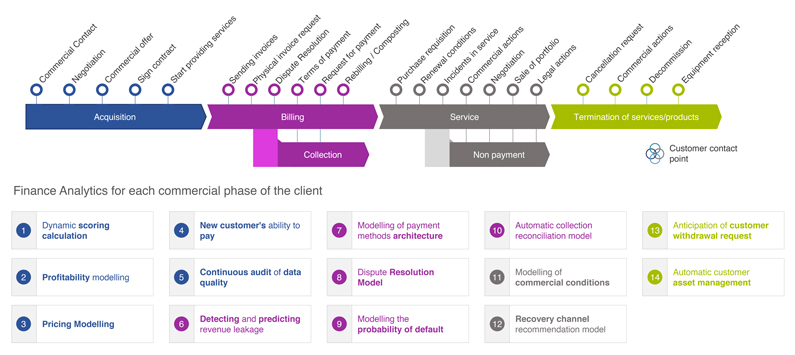

Default payment analytics

To meet the needs 2 and 3, in everis, from our CoE of collection management, leveraged on technology, we have designed 14 analytical models throughout the life of the client in the company with the aim of

- Securing income

- Optimize recovery actions

- Improving DSO

- Process efficiency

In addition, the end-to-end vision of the customer enables the reuse of statistical information and the search for synergies between cases of use (e.g., actions aimed at charging for the service before non-payment in advance).

The 14 use cases developed have been grouped into the four phases of the customer’s business cycle with different objectives:

- Acquisition: the future behaviour of the customer is predicted, both in terms of payment capacity and profitability, enabling the allocation of more efficient commercial actions on customers with higher potential returns.

- Invoicing and Collection: ensure correct invoicing and homogenize the response to possible disputes.

- Service: efficiency initiatives in commercial management, such as the improvement of commercial conditions to retain and build customer loyalty. With these solutions, we will predict when a customer will fall into arrears, and help the collection department decide what the best action is to achieve recovery.

- Churn: models that predict if a customer is going to cancel the acquired services, allowing the sales team to anticipate and offer new commercial conditions to avoid the leakage.

Use cases are tested, validated and quantified by everis before they are incorporated into the client’s BAU in a short period of time of ~ 10 weeks. Where our clients are obtaining improvements in their recovery management ratios such as:

- Insurance: An annual savings in policy non-payment and associated claims of 3M.

- Telecom: 70% of the amount recovered through the action on 50% of the defaulters.

- Utilities: more than 10 customized actions to reduce customer leakage.

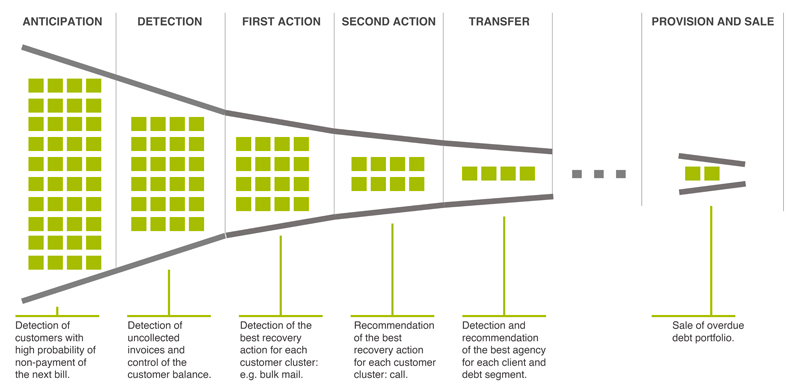

Funnel example of recovery actions generated by the algorithms.

In a demand shock like the one we are facing and with the huge default wave that is coming, successful companies will be the ones that get it:

- Ensure business continuity, stabilize processes as a starting point before reviewing and optimizing them.

- Shielding clients, the acquisition of new clients can cost up to 7 times more than the retention and maintenance of our portfolio.

- Predicting and prescribing personalized recovery actions, as a measure to increase the success rate of the actions.